Based on standard metrics, a breathtaking and persistent valuation gap exists between stocks in Japan and China. For the last 10 years (and likely more), Japan has been a perennial deep value market while China has been an overpriced growth market.

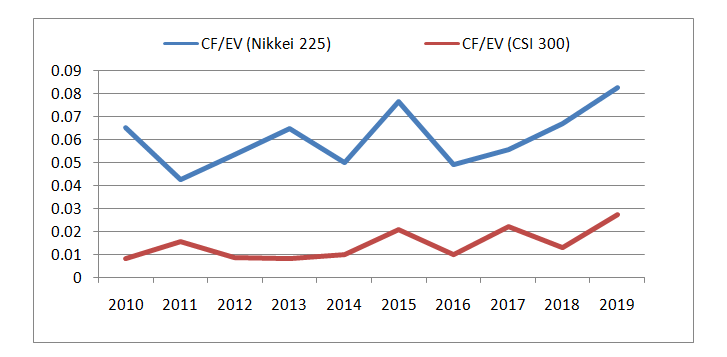

In Figure 1, we see a wide and persistent gap between the average cash flow to enterprise value (“CF/EV”) ratio of all stocks in the Nikkei 225 Index (Japan) versus those of the CSI 300 Index (China). These indexes are representative baskets of large market capitalization stocks in the two countries. As enterprise value is the sum of market capitalization and debt, value stocks tend to have higher CF/EV ratios owing to a lower EV.

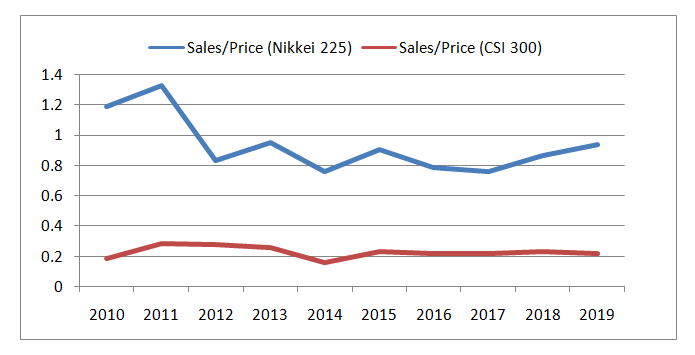

In Figure 2, we see a wide and persistent gap between the average sales-to-price of all stocks in the Nikkei 225 Index versus those of the CSI 300 Index. Growth stocks tend to have lower sales-to-price ratios because prices are higher as they price in higher sales in the future.

What is the reason for this gap? Of course, overpriced stocks in China are hardly a surprise. But if China has been the quintessential growth story for the past three decades, then what happened in Japan? What collective psychology led to such depressed valuations for such a long time?

If, like me, you stayed in the Tokyo Imperial Hotel in the late 1980s, you would know that once upon a time, Japan had amassed the world’s largest fortune1. It had the world’s largest stock markets in terms of market capitalization, surpassing New York. Its banks were the world’s largest too, clinching nine of the top ten spots.

It was said then that the land beneath the Imperial Palace in Tokyo was worth more than the whole State of California. The market value of the country’s assets, including real estate, exceeded that of the United States.

As the export juggernaut to the world, it became the largest foreign holder of U.S. Treasuries. Punitive tariffs were imposed on its exports to the U.S., leading to prolonged trade tensions.

Clearly, much has changed since the days of “Japan As Number One” 2 and “The Japan That Can Say No” 3. Years of speculation and over-confidence, coupled with easy money and unchecked credit expansion, led to a huge economic bubble that finally burst in the 1990s 4. The collapse precipitated a “Lost Decade” (or two or three) of economic stagnation and deflation that lasted until today.

The impact of the collapse on businesses and households was immense – none more than on the confidence to invest again. One cannot imagine the scale of the collapse until one realizes, for example, that by the early 2000s, property in prime districts in Tokyo had slumped to less than 1% of their peak values but still managed to list as the world’s most expensive at the time.

The Japanese were burned – no, incinerated – and they became extremely conservative. Japan now teems with listed companies with extremely strong balance sheets, stable cash flows and little or no debt – with not much of a market capitalization to show for these admirable characteristics. It is like they keep accumulating cash but are too fearful to spend it.

This is the reason Japan has been such an enduring deep value market.

Indeed, it is an inside joke that if you could transport a Japanese company to China, its market value would triple overnight by virtue of its balance sheet alone. To the savvy entrepreneurs and investors who are able to connect the products and capital resources of Japanese companies to the growth opportunities in China, this is a vast arbitrage opportunity. Practically, it involves adopting an activist approach to investing in Japan, in which management scarred by decades of stagnation and fearful of investing must be prodded into reaching out globally once again 5.

References:

1. Murphy, R.T. “Power Without Purpose: The Crisis of Japan’s Global Financial Dominance”, Harvard Business Review, March-April 1989.

2. Vogel, E.F. “Japan as Number One”, Harvard University Press, 1979

3. Morita, A. and Ishihara, S. “The Japan That Can Say No”, Tokyo: Kobunsha, Kappa-Holmes, 1989

4. Fujii, M and Kawai, M. “Lessons from Japan’s Banking Crisis, 1991-2005”, Asian Development Bank Institute Working Paper Series, No. 222, June 2010

5. Some content in this post was published in a HFM marketing article about Auspicious Capital Management, Hong Kong (disclosure: I work for this company).